As an example, if a residential or commercial property has a value of $200,000 and the insurance service provider needs an 80% coinsurance, the owner needs to have $160,000 of property insurance coverage. Owners might consist of a waiver of coinsurance clause in policies. A waiver of coinsurance provision gives up the property owner's requirement to pay coinsurance.

In many cases, however, policies may consist of a waiver of coinsurance in case of a total loss. Coinsurance is the quantity a guaranteed need to pay versus a medical insurance claim after their deductible is pleased. Coinsurance also uses to the level of property insurance that an owner should buy on a structure for the coverage of claims.

Both copay and coinsurance arrangements are ways for insurer to spread out risk among individuals it guarantees. Nevertheless, both have advantages and disadvantages for consumers.

Many or all of the items featured here are from our partners who compensate us. This might affect which items we write about and where and how the item appears on a page. However, this does not influence our assessments. Our viewpoints are our own. Medical insurance differs from any other insurance you purchase: Even after you pay premiums, there are complicated out-of-pocket expenses like deductibles, copays and coinsurance.

It is very important to understand the essentials of health insurance coverage so you can make the best financial choices for your household prior to Find more info you require care. how much does it cost to go to the dentist without insurance. That way, you can focus more on healing when the time comes. Here's our guide on how the costs of health insurance coverage work. Prior to you comprehend how all of it interact, let's brush up on some typical health insurance coverage terms.

Like a gym subscription, you pay the premium each month, even if you do not use it, otherwise lose coverage. If you're fortunate sufficient to have employer-provided insurance, the company typically selects up part of the premium. A fixed rate you pay for health care services at the time of care.

The deductible is just how much you pay before your medical insurance begins to cover a larger portion of your expenses. In general, if you have a $1,000 deductible, you need to pay $1,000 for your own care out-of-pocket before your insurer begins covering a greater portion of costs. The deductible resets yearly.

How Much Is Birth Control Without Insurance Fundamentals Explained

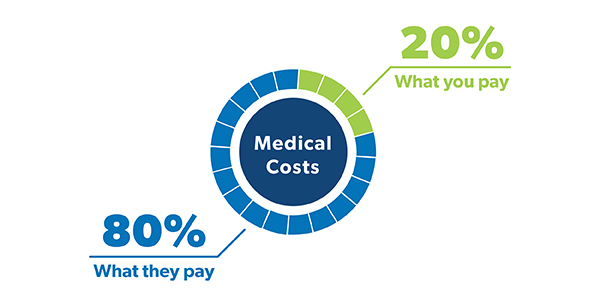

For example, if you have a 20% coinsurance, you pay 20% of each medical bill, and your medical insurance will cover 80%. The most you might need to pay in one year, out of Continue reading pocket, for your healthcare prior to your insurance covers 100% of the bill. Here you can see the maximums enabled by the government for personal prepare for this year.

Some policies have low premiums and high deductibles and out-of-pocket maximum limits, while jobs selling timeshares others have high monthly rates and lower deductibles and out-of-pocket limitations. In basic, it works like this: You pay a regular monthly premium just to have health insurance coverage (how to apply for health insurance). When you go to the physician or the health center, you pay either full cost for the services, or copays as laid out in your policy.

The staying percentage that you pay is called coinsurance. You'll continue to pay copays or coinsurance up until you've reached the out-of-pocket maximum for your policy. At that time, your insurance provider will begin paying 100% of your medical costs up until the policy year ends or you change insurance coverage plans, whichever is initially.

If you utilize an out-of-network medical professional, you could be on the hook for the whole expense, depending upon which kind of policy you have. This brings us to three new, related definitions to comprehend: The group of medical professionals and providers who agree to accept your health insurance coverage. Health insurance providers work out lower rates for care with the physicians, health centers and clinics that are in their networks.

If you get care from an out-of-network company, you may have to pay the entire bill yourself, or simply a part, as indicated in your insurance policy summary. A provider who has actually accepted work with your insurance coverage plan. When you go in-network, your expenses will generally be cheaper, and the costs will count toward your deductible and out-of-pocket maximum.

Your expenses would be different based upon your policy, so you'll wish to do your own estimations each year when facing a medical cost. Vigilance is single and has a yearly deductible of $1,200. Her insurance coverage plan has some copays, which do not count toward her deductible. After she fulfills the deductible, her insurer pays 80% of her medical bills, leaving Vigilance with coinsurance of 20%.

Because she goes to an in-network service provider, this is a totally free preventive care see. Nevertheless, based upon her physical, her medical care physician thinks Vigilance ought to see a neurologist, and the neurologist advises an MRI. Copays for an in-network expert on her plan are $50, which she needs to pay, while her insurance provider will cover the rest of the neurologist's charge.

Some Known Facts About How To Get Cheap Car Insurance.

Imaging scans like this are "subject to deductible" under Prudence's policy, so she should pay for it herself, or out-of-pocket, due to the fact that she hasn't met her deductible yet. So her insurance provider will not pay anything to the MRI center. $50 for the neurologist copay + $1,000 for the scan = $1,050. Later in the year, Vigilance falls while treking and injures her wrist.

After the copay, ER charges were $3,400. Her deductible will be applied next. Prudence paid $1,000 of her $1,200 deductible earlier in the year for her MRI, so she is accountable for $200 of the ER costs before her insurer pays a larger share. After deductible and copay, the ER charges total $3,200.

$ 100 for the ER copay + $200 for staying deductible + 20% coinsurance ($ 640) = $940. Prudence has actually now paid $1,990 toward her medical costs this year, not consisting of premiums. She has actually also satisfied her annual deductible, so if she requires care again, she'll pay only copays and 20% of her medical expenses (coinsurance) up until she reaches the out-of-pocket optimum on her plan.

Comprehending health care can be complicated. That's why it's practical to know the meaning of commonly utilized terms such as copays, deductibles, and coinsurance. Understanding these important terms might assist you understand when and how much you need to pay for your healthcare. Let's have a look at the definitions for these three terms to better understand what they indicate, how they work together, and how they are different.

For example, if you injure your back and go see your medical professional, or you need a refill of your child's asthma medicine, the quantity you pay for that visit or medication is your copay. Your copay quantity is printed right on your health strategy ID card. Copays cover your portion of the expense of a doctor's go to or medication.

Not all plans use copays to share in the expense of covered expenses. Or, some plans may use both copays and a deductible/coinsurance, depending on the type of covered service. Likewise, some services may be covered at no out-of-pocket cost to you, such as yearly checkups and particular other preventive care services. * A is the quantity you pay each year for the majority of qualified medical services or medications before your health plan begins to share in the expense of covered services. how much does it cost to go to the dentist without insurance.