Term life insurance coverage is attractive to young individuals with children. Parents may acquire large quantities of coverage for fairly low expenses. Upon the death of a moms and dad, the considerable Go to this website advantage can change lost income. These policies are also well-suited for people who momentarily need specific quantities of life insurance coverage. For instance, the policyholder may compute that by the time the policy ends, their survivors will no longer require additional monetary protection or will have collected enough liquid properties to self-insure.

The ideal option for you will depend on your requirements; here are some things to consider. Term life policies are ideal for people who desire considerable coverage at low expenses. Entire life consumers pay more in premiums for less protection however have the security of knowing they are safeguarded for life.

Upon renewal, term life insurance coverage premiums increase with age and might end up being cost-prohibitive in time. In reality, renewal term life premiums may be more pricey than permanent life insurance premiums would have been at the problem of the initial term life policy. Unless a term policy has ensured eco-friendly policy, the business might decline to renew coverage at the end of a policy's term if the policyholder developed a serious health problem.

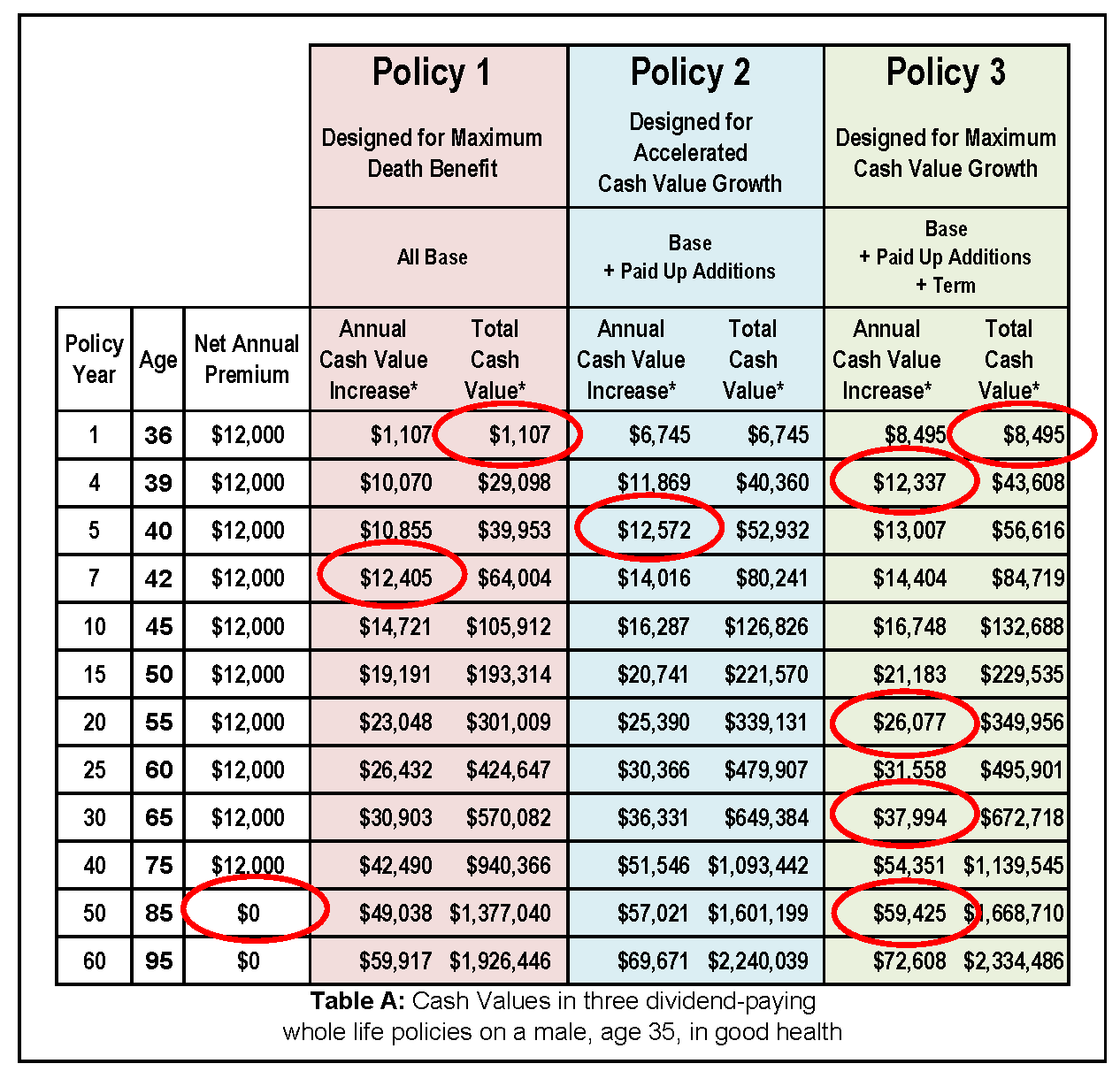

Some customers choose permanent life insurance coverage because the policies can have an investment or cost savings vehicle. A portion of each premium payment is assigned to the cash value, which may have a growth assurance. Some plans pay dividends, which can be paid or continued deposit within the policy.

The 9-Second Trick For How Much Does An Eye Exam Cost Without Insurance

There are also numerous distinct tax advantages, such as tax-deferred cash value growth and tax-free access to the money part. Financial advisors warn that the growth rate of a policy with cash worth is often paltry compared to other monetary instruments, such as shared funds and exchange-traded funds (ETFs). Likewise, substantial administrative fees frequently cut into the rate of return.

Apparently, there is no one-size-fits-all answer to the term versus irreversible insurance debate. Other aspects to consider consist of: Is the rate of return made on Hop over to this website financial investments adequately attractive?Does the long-term policy have a loan provision and other features?Does the policyholder have or plan to have a business that needs insurance coverage?Will life insurance coverage contribute in tax-sheltering a sizable estate? Convertible term life insurance coverage is timeshare debt collection laws a term life policy that includes a conversion rider.

The conversion rider need to permit you to transform to any long-term policy the insurance business uses with no limitations. The primary functions of the rider are keeping the original health rating of the term policy upon conversion, even if you later have health concerns or end up being uninsurable, and deciding when and how much of the protection to transform.

Naturally, total premiums will increase considerably, given that entire life insurance is more costly than term life insurance coverage. The advantage is the guaranteed approval without a medical examination. Medical conditions that establish throughout the term life period can not change premiums upward. However, if you wish to add extra riders to the brand-new policy, such as a long-term care rider, the company may require restricted or complete underwriting.

All about How To Find A Life Insurance Policy Exists

" Life insurance coverage is method too complicated! I'll fret about it when I'm older." We've all had comparable thoughts. Let's face it, everybody zones out of those life insurance commercials because they're ridiculously uninteresting. But stick with us and we'll reveal you why term life insurance is the finest life insurance coverage option.

If you pass away prior to the term is over, the insurer will pay the survivor benefit (another way to say payment). If you die after the term is over, the insurer doesn't pay. We suggest buying a term policy that lasts 1520 years. You require life insurance coverage if you have a family or loved ones who depend on your incomebecause no one lives forever.

It's not a good thing to believe about, we concur. But taking the time to figure it all out now is a million times smarter than leaving your enjoyed ones stranded if you all of a sudden died. Term life insurance coverage works just like your cars and truck or home insurance coverage with a regular monthly payment, aka a premium.

Steve's survivor benefit is $400,000 due to the fact that we suggest getting protection that's 1012 times your annual income. If he dies before his 20-year term is over, the $400,000 will go to his beneficiaries (his spouse and 2 kids). Although a beneficiary is probably to be a liked one, it might also be legal guardians, your estate, a charity, or a legal trust.

Not known Incorrect Statements About Why Is Car Insurance So Expensive

But that's a great deal of premiums to payand high ones at that! We're talking 5-10 times more than a term life premium. Why are whole life premiums so high? Due to the fact that whole life insurance tries to imitate a financial investment fund (together with others in the money value insurance household). Part of the sales pitch for money value kinds of insurance is that they'll help you develop an investment that might be tapped into even more down the line.

In truth however, when it comes to the "making money" part. Let's return to our great friend Steve. He likes to meddle the stock exchange, but his insurance agent says if he opts for whole life insurance, his premium will cover his life insurance policy and include investing.

That's due to the fact that the rates of return for entire life insurance policies are compared to the rate of return in something like a mutual fund. Regrettably, "riders" have nothing to do with horses or motorbikes in the interesting world of insurance coverage. Riders are additionals that "trip" on your routine term policy to function as a response to "what if" questions like: What if we need to cover unforeseen funeral service expenditures for a family member? What if I become handicapped and can't pay my premium? One rider that may be worth having is one that covers funeral costs for your child.

And the reality is, other concerns can also be covered by building an emergency fund of cost savings through. Get that going, and you'll generally develop your own "rider" or cushion just by saving and taking control of your cash. You don't need to throw cash away to spend for a rider you don't need.

5 Easy Facts About How Much Does Flood Insurance Cost Described

If you are nearing the end of the regard to your policy, you might constantly restore the policy for another term. If you have a "level term" type of plan (more on the types quickly) then your premium rate will increase when you restore (as you'll be older and more costly to guarantee).

However you must ultimately strive being self-insured with an emergency situation fund by the time your policy ends. It's simpler than you think! If you put 15% of your family income toward investing, you won't need the death benefit by the time your term life plan ends due to the fact that you'll have made a quite penny in financial investments (how to get health insurance after open enrollment).